First and foremost, what is human capital? It is in my opinion, the present value of what it is you have the potential to earn from paid employment and/ or entrepreneurship. So say you are a fresh graduate, your potential income until retirement from the use of your mental faculty as well as your physical abilities combine to form your human capital.

{kind=link}

So why does this matter? What I have learned from my days on this planet is that your total wealth consists of both your human capital and financial capital (a discussion for another session). In light of this, it can be said that once you start working (as a fresh employee or “green horn”), your human capital is at the highest but then again prior to this, you are in the “gathering” or “accumulation” phase of your life (for those of us that did not get millions of cash from daddy or mummy). We must act as a sponge – just absorbing all the knowledge and information that we can lay our hands on, it is critical!

It is this information that will help us build our retirement portfolios and future wealth. This is why we should not overlook our human capital because as we grow older, our human capital does reduce while our financial capital (should) increase. So why is this the case?

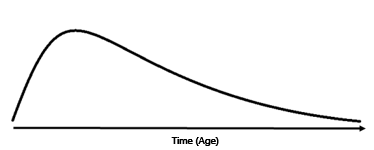

Below is an attempt at describing the trend of human capital. The chart shows the way human capital evolves in time – it resembles a shape that statisticians and mathematicians may be familiar with…

Imagine this. Who do you think an employer will hire to carry out manual heavy lifting? A man of 50 years or a man of 25 years? In many cultures (Nigeria included), one cannot send an elder to do manual labour while there are “small boys” the same age as his children. Right?

The 50-year-old man will most likely not be hired for that role – let’s call a spade a spade! Although the 50-year-old man’s human capital has declined as shown in the chart above, his human capital will never get to zero (0) unless he dies. However, he should start preparing to hand over to the “new boys and girls” (as they apply) because this is also part of retirement planning – the cycle of life you may say.

That said, if you are a regular salaried employee, I encourage you to try to take risks while you are young – of course, calculated risk. Invest, take chances because when you grow older with more responsibilities, you may find that there is no time to take those risks or the risks begin to seem very hazardous which may find you getting desperate.

So ladies and gentlemen when you start working, begin to plan for your own retirement by capitalising on your human capital – your investment path because that is all you have when you start your career. We shall go into what kinds of investments you could look into to build your retirement savings in another post.

Until then, do remember that there is nothing really 100% guaranteed.